Why Wrong-Way Risk Is Worse Than We Admit

Part 4 - Exposure peaks exactly when counterparty capacity weakens. The hedge protects until the hedger can't pay. Collateral secures until it's what keeps the borrower alive. Standard models assume independence; wrong-way risk means severe correlation nobody's pricing.

📊 EMERGING RISKS SERIES: What I'm Watching Now — Part 4 of 5

This post is part of a series on current risk patterns that concern an experienced CRO.

In this post: why exposure peaks exactly when counterparty capacity weakens—and why standard models consistently underestimate this structural vulnerability.

There’s a pattern in institutional risk that makes me increasingly uneasy.

Not because it’s new—it’s been present for decades. But because I’ve watched it become more concentrated, more structurally embedded, and more uncomfortable to name.

Wrong-way risk.

The situation where your exposure to a counterparty is largest exactly when their capacity to meet that obligation is weakest.

The hedge that protects you is provided by the entity least able to pay when the hedge is needed. The collateral securing your loan is the same asset keeping the borrower solvent. The dependency you’ve built into your operations concentrates exactly where failure would hurt most.

It’s not bad luck. It’s structure.

And the institutions that understand this well aren’t the ones with the most sophisticated models. They’re the ones willing to ask uncomfortable questions about relationships, strategies, and dependencies that leadership may already be committed to.

What Makes It Wrong Way

Wrong-way risk appears when what you’re exposed to and what keeps the counterparty viable are the same thing.

An airline hedges fuel costs with an oil producer. When oil prices spike, the hedge moves in the airline’s favor—but the producer’s credit quality deteriorates under the same conditions.

A property developer borrows against their own development portfolio. When property values fall, both the collateral and the borrower’s capacity to repay deteriorate simultaneously.

A derivatives counterparty whose business model depends on rates staying stable provides you with rate protection. When rates move sharply, your exposure to them peaks exactly as their viability comes under pressure.

This isn’t a failure of credit analysis. It’s a feature of how the relationship is structured. And it shows up in more places than most institutions acknowledge.

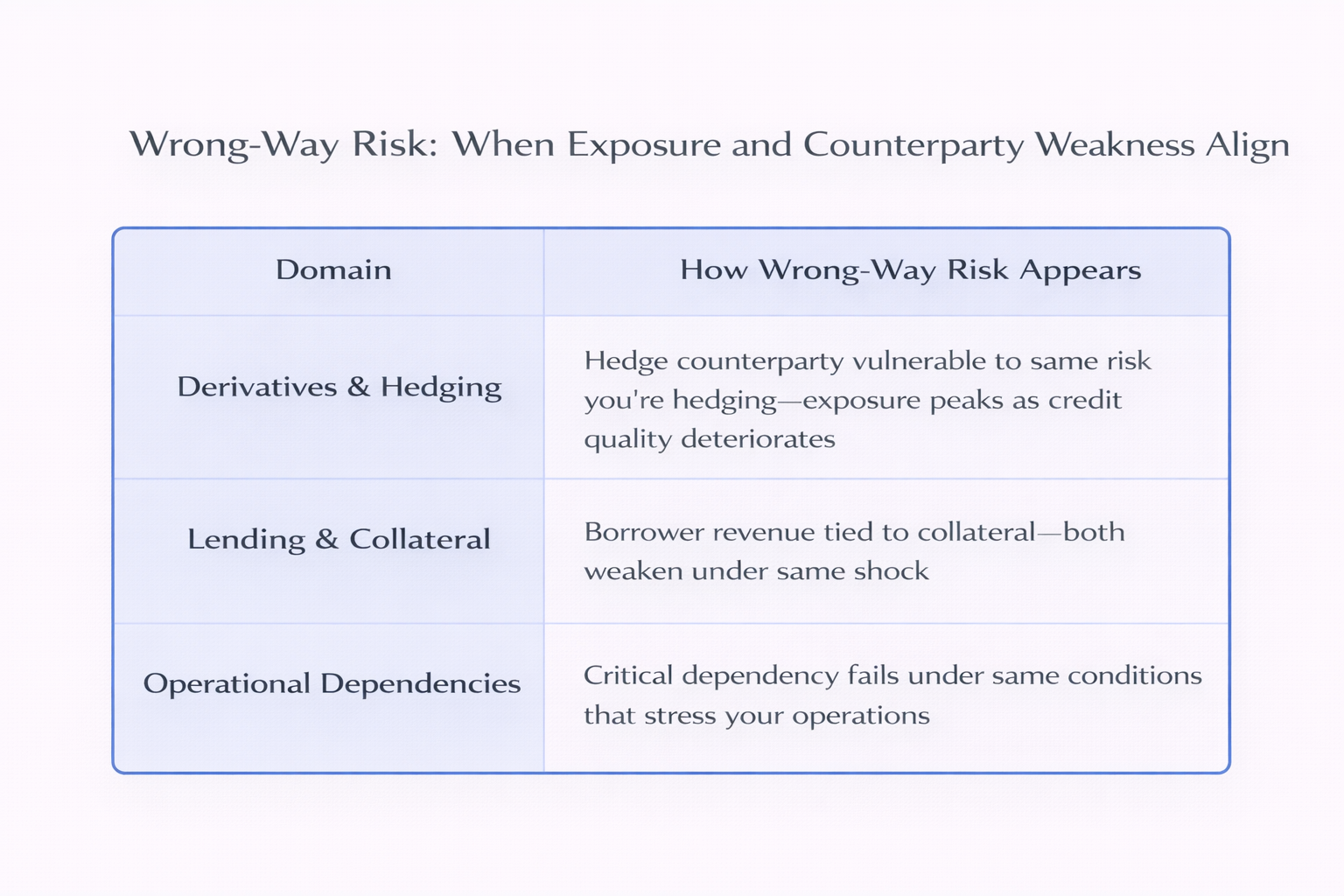

Where It’s Structurally Embedded

I’ve watched wrong-way risk appear across three domains—and in each case, it’s treated as manageable until stress reveals it wasn’t.

In derivatives and hedging. The counterparty providing your hedge is often economically sensitive to the same risk you’re hedging. Interest rate swaps with banks whose funding costs move with rates. FX forwards with corporates whose revenue depends on currency stability. Commodity hedges with producers whose survival depends on price levels.

When the risk materializes, two things happen at once: your exposure increases (the hedge moves in your favor) and counterparty credit quality deteriorates (they’re hurt by the same move). Standard credit models assume these move independently. Wrong-way risk means they’re correlated—often severely.

In lending and collateral. Borrowers whose revenue is tied to the collateral securing the loan. Energy producers borrowing against reserves. Real estate developers secured by their own projects. Exporters borrowing against receivables denominated in the currency that’s now under pressure.

The structure looks sound when collateral values are stable. But when stress hits, the collateral depreciates at the same time the borrower’s capacity to repay weakens. Loss given default isn’t just about recovery rates—it’s about the fact that default and loss severity are driven by the same shock.

In operational dependencies. Vendors, suppliers, or service providers whose failure would cascade through your operations. A single cloud provider. A concentrated payments processor. A critical correspondent bank in a key corridor.

These are often treated as “operational risk” or “business continuity” issues. But they’re also counterparty credit risk with severe wrong-way characteristics. The conditions that stress your operations (cyber incident, geopolitical shock, regulatory action) are often the same conditions that stress the dependency you’ve built.

Why Models Understate It

Standard credit models are built on an assumption: counterparty default probability and exposure at default move independently.

That assumption breaks down completely under wrong-way risk.

Potential Future Exposure (PFE) is typically calculated using unconditional market distributions. It asks: “How large could this exposure get?” But it doesn’t ask: “How large is it likely to be if the counterparty actually defaults?”

Those are different questions. And for wrong-way risk, the second question produces far larger numbers.

Credit Valuation Adjustment (CVA) is supposed to account for counterparty credit risk in derivatives pricing. But most CVA models either ignore wrong-way risk entirely or treat it as a modest adjustment. When wrong-way correlation is explicitly modeled, expected exposure can jump by multiples—not percentage points.

I’ve seen institutions where the PFE at 95% confidence suggested modest residual risk, well within risk appetite. Then a concentrated, wrong-way exposure materialized under stress, and realized losses ran to multiples of what the models indicated. Not because the models were badly calibrated—because they were measuring the wrong thing.

Why It’s Uncomfortable To Surface

Wrong-way risk is structurally embedded in relationships and strategies that leadership may already be committed to.

Naming it explicitly means acknowledging that:

A key hedging relationship carries fragility that can’t be hedged away. The institution providing your protection is vulnerable to the same risk you’re protecting against—and there may not be a better alternative available.

A lending strategy concentrates credit and collateral risk in ways that standard metrics don’t capture. Growth in the portfolio isn’t just adding exposure—it’s compounding structural vulnerability.

An operational dependency creates single points of failure that can’t easily be diversified. The efficiency gained from consolidation comes with concentration risk that governance hasn’t fully priced.

These aren’t comfortable conversations. Especially when the relationships are strategic, the strategies are generating returns, and the dependencies are deeply embedded in operating models.

But ignoring wrong-way risk doesn’t make it go away. It just means the institution discovers it under the worst possible conditions—when stress has already arrived and options have already narrowed.

What Changes When You See It

Recognizing wrong-way risk doesn’t eliminate it. Some structures genuinely are the best available option, even with embedded fragility.

What changes is how you govern it.

The institutions that manage this well don’t pretend wrong-way risk is an edge case. They name it explicitly. They stress-test it under conditions where exposure and counterparty weakness move together. They price it into capital buffers as a structural feature of the relationship—not as an afterthought.

And they accept that sometimes, the right answer is to cap exposure, diversify dependencies, or decline relationships—even when those choices are commercially unattractive.

📌 Key Takeaways:

- 1️⃣ Wrong-way risk is structural, not incidental—exposure peaks when counterparty weakens because revenue, survival, or viability is tied to the same risk you’re hedging or financing.

- 2️⃣ Standard models assume counterparty default and exposure move independently; wrong-way risk means they’re correlated, often severely, making PFE and CVA dramatically understate true risk.

- 3️⃣ Appears in derivatives (hedges tied to hedger survival), lending (collateral = borrower revenue source), and operational dependencies (single points of failure).

- 4️⃣ Uncomfortable to surface because it challenges relationships leadership is committed to and implies accepting less attractive alternatives or capping strategically important exposures.

- 5️⃣ Recognizing wrong-way risk doesn’t eliminate it—it means naming it explicitly, stress-testing under correlated conditions, and governing it as structural vulnerability rather than edge case.

Wrong-way risk is uncomfortable to surface because acknowledging it means admitting that some structures carry fragility that can’t be hedged away.

Frequently Asked Questions

For readers seeking clarity on identifying and governing wrong-way risk:

What’s the difference between general, specific, and leveraged wrong-way risk?

General wrong-way risk is broad market/credit linkage—an airline hedging fuel with an oil producer (both affected by oil prices but not directly dependent). Specific wrong-way risk is legal or structural linkage—a company buying options on its own stock (counterparty exposure directly tied to underlying). Leveraged wrong-way risk is when portfolio value directly determines counterparty viability—a hedge fund whose survival depends on the positions you’re financing. Most institutions focus on specific WWR; the larger blind spot is recognizing when general WWR has become structural.

Why don’t standard credit models capture wrong-way risk adequately?

Because they assume counterparty default probability and exposure at default move independently. Potential Future Exposure (PFE) uses unconditional market distributions—it asks “how large could exposure get” not “how large when the counterparty defaults.” Credit Valuation Adjustment (CVA) is supposed to account for this but most models either ignore wrong-way correlation or treat it as a modest adjustment. When wrong-way correlation is explicitly modeled, expected exposure can jump by multiples—the gap between unconditional and conditional distributions is where the blind spot lives.

How does wrong-way risk show up outside of derivatives?

In lending: borrowers whose revenue is tied to collateral (property developers secured by their projects, energy producers against reserves, exporters with FX-denominated receivables). In operational dependencies: vendors or service providers whose failure would cascade (single cloud provider, concentrated payment processor, critical correspondent bank). These are often treated as operational or business continuity risk, but they’re counterparty credit risk with severe wrong-way characteristics—the shock that stresses your operations also stresses the dependency.

What should risk functions do when wrong-way risk is embedded in strategic relationships?

Don’t pretend it’s an edge case or technical adjustment. Name it explicitly in credit proposals and risk appetite discussions. Stress-test under conditions where exposure and counterparty weakness move together—not independently. Price it into credit decisions and capital buffers as a structural feature, not an afterthought. Recognize that “fully hedged” can create false comfort if the hedge itself carries correlated counterparty risk. Accept that sometimes the right answer is to cap exposure, diversify dependencies, or decline relationships—even when commercially unattractive.

Next in series: What Recognizing Risk Early Actually Looks Like—practitioner patterns for seeing risks before they show up in formal metrics, and the discipline of watching without waiting for dashboards to confirm what you already sense.

Posts like this are written for risk professionals who need to see patterns before metrics confirm them. Subscribe to receive new posts from The Risk Philosopher directly.

Related Reading:

- Part 3 - The Quiet Withdrawal of Liquidity Providers

- Part 2 - Geopolitics Is No Longer a Scenario

- Part 1 - Why I’m Concerned About Correlation Regimes

The exposure you’re most confident about is often the one most vulnerable to the failure you least expect.