The Quiet Withdrawal of Liquidity Providers

Part 3 - Liquidity providers withdraw incrementally through behavioral shifts metrics miss: selective spread widening, correspondent de-risking, conditional depth. Markets quote prices until institutions need execution at size—then discover relationships changed while dashboards still showed green.

📊 EMERGING RISKS SERIES: What I'm Watching Now — Part 3 of 5

This post is part of a series on current risk patterns that concern an experienced CRO.

In this post: behavioral shifts in liquidity provision that don't show up in standard metrics—and why markets look liquid until you actually need depth.

For the past year, I’ve been watching liquidity behave in ways that standard metrics don’t capture.

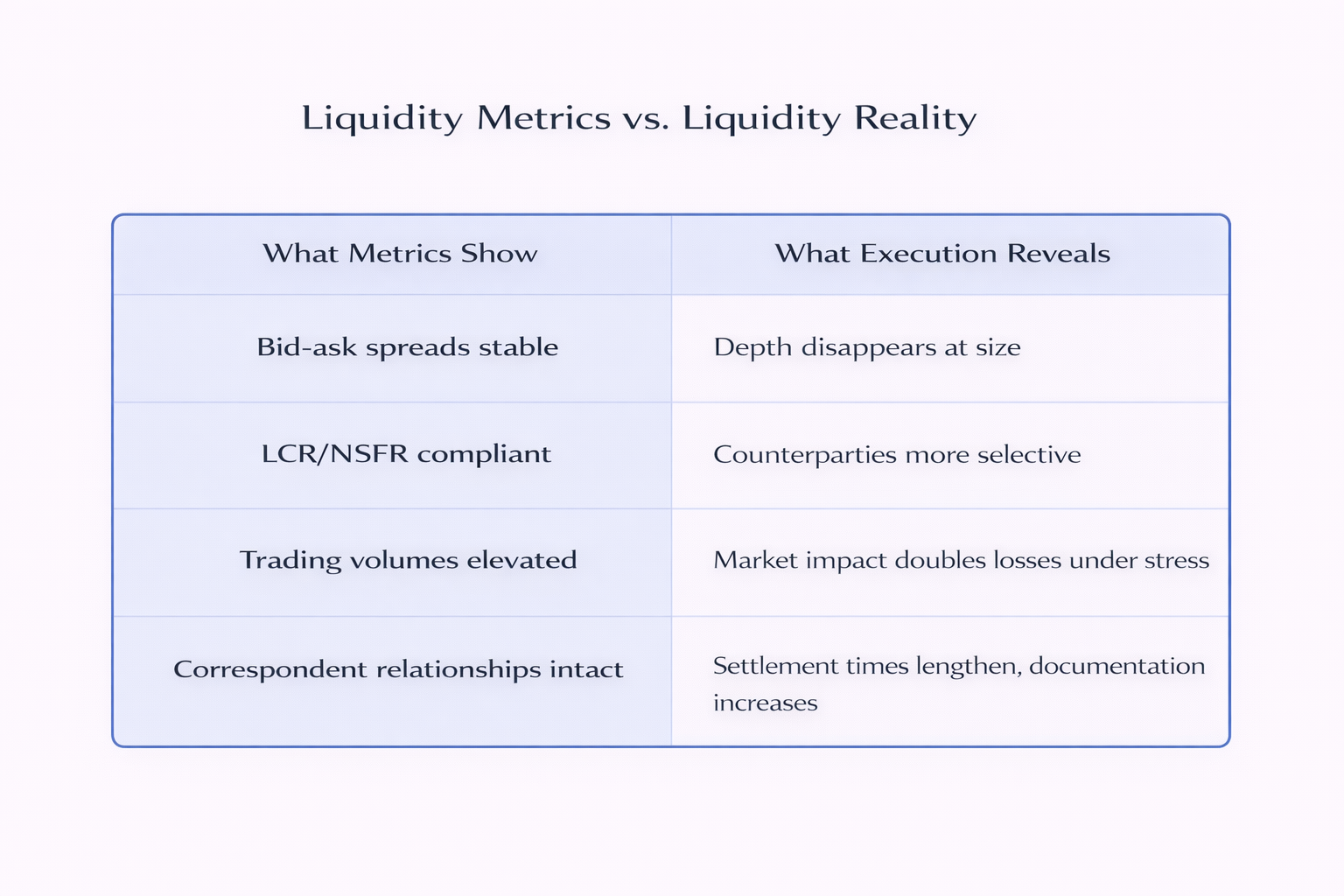

Markets quote prices. Spreads look normal. Depth appears adequate. Trading volumes stay elevated.

But when institutions try to execute at size—especially under pressure—they’re discovering something has quietly changed. Not in the formal market structure, but in the behavior of those who provide liquidity.

Market-makers are stepping back faster. Correspondent banks are reassessing relationships. Depth that existed on screens disappears when you actually try to trade.

This isn’t a liquidity crisis in the traditional sense. There’s no freeze, no dramatic headline, no regulatory intervention required.

It’s something more subtle and more consequential: a behavioral withdrawal that happens incrementally, rationally, and almost invisibly—until the moment you need liquidity and discover the assumptions you built on no longer hold.

Why This Is Different

What I’m watching is behavioral, not structural. The infrastructure still works. The systems still function. What’s changing is how providers choose to use that infrastructure—more selective about when, how, and for whom they provide liquidity.

It’s incremental, not sudden. A market-maker reduces inventory by 20%. A correspondent bank tightens documentation for certain corridors. A dealer widens spreads for specific clients by 10 basis points. Each move is individually rational and barely noticeable. Collectively, they reshape market liquidity without triggering any formal threshold.

And it shows up in execution, not in metrics. Bid-ask spreads look stable. LCR ratios stay green. Trading volumes don’t collapse. But when you try to execute a position at size, you discover the depth was conditional—and the conditions just changed.

Where I’m Seeing The Withdrawal

The pattern shows up in ways that feel like isolated operational friction—until you recognize they’re part of a broader shift.

Market depth that exists until you test it. I’ve watched institutions where bid-ask spreads looked normal right up until they needed to execute above a certain threshold. What appeared as two-way pricing at modest size disappeared at scale. The market didn’t freeze—it just wasn’t there for the size they needed, when they needed it.

Correspondent banks de-risking selectively. Correspondent banking relationships that functioned smoothly for years are being quietly reassessed. Not wholesale exits—targeted adjustments. Certain corridors require more documentation. Certain client types face longer settlement times. Certain currencies become harder to clear.

None of this shows up as a relationship termination. It shows up as friction—slightly higher costs, slightly longer timelines, slightly more scrutiny. But friction compounds. And when stress hits, what used to be a reliable route becomes constrained exactly when you need it most.

Market-makers managing inventory more tightly. I’ve seen market-makers who used to carry meaningful inventory now operate with much thinner books. They’re still quoting. They’re still providing two-way markets. But they’re doing it with less capital committed, which means less capacity to absorb large or sudden flows.

This makes perfect sense from a capital efficiency perspective. But the aggregate effect is that market capacity to absorb stress has quietly diminished—while measures of market functioning still look fine.

What’s Driving The Behavior

Three forces are making liquidity provision more conditional, and they’re all intensifying.

Geopolitical fragmentation is making relationships conditional. Liquidity providers are reassessing counterparty and corridor risk through a geopolitical lens. Jurisdictions that felt stable now carry ambiguity. Relationships that were automatic now require judgment calls. Routes that were open now depend on political alignment that may not hold.

The willingness to provide liquidity becomes more selective, more expensive, and more conditional on factors that have nothing to do with credit quality or market volatility.

Regulatory ambiguity is creating ambiguity costs. When regulatory expectations are shifting, diverging across jurisdictions, or open to interpretation, providers don’t know what will be challenged, when, or by whom.

The rational response is to reduce exposure where ambiguity is highest—pulling back from clients, products, or corridors where regulatory scrutiny might intensify, even if nothing has formally changed yet.

Capital efficiency pressures are reducing marginal support. In an environment where capital is expensive and returns are compressed, every dollar of balance sheet dedicated to liquidity provision is a dollar not deployed elsewhere.

Providers are optimizing. They’re still supporting core clients and core markets. But marginal clients, tail-risk products, and less liquid markets are seeing less support—not because providers can’t provide liquidity, but because the return on capital no longer justifies it.

The system still looks liquid for average transactions in normal times. But capacity to absorb large, stressed, or unusual flows has diminished—and won’t be visible until those flows actually materialize.

Why Governance Misses This

Behavioral liquidity withdrawal happens upstream of where standard metrics look.

Metrics measure outcomes, not behavior. LCR tells you whether you can survive a 30-day stress. It doesn’t tell you whether counterparties will still transact with you on day 15. Bid-ask spreads tell you what dealers quote at modest size. They don’t tell you what happens when you need to move a position ten times larger.

A correspondent bank doesn’t announce it’s de-risking a corridor. It just starts asking more questions, processing transactions more slowly, requiring more documentation. A market-maker doesn’t publicly reduce inventory. It just quotes tighter size limits or steps away during volatility.

By the time these shifts show up in formal liquidity metrics, the withdrawal is already well advanced.

And execution risk doesn’t show up in mark-to-market. Positions are valued using market prices that assume you can transact at those prices. For concentrated positions or stressed markets, that assumption often doesn’t hold.

I’ve watched institutions discover that a position valued at X became worth substantially less the moment they tried to exit—not because the market moved, but because their own act of selling moved it. When you’re forced to sell quickly in a market that’s already stressed, liquidity impact can easily double the loss.

What This Means

The practitioners who aren’t surprised by this don’t have better liquidity models. They watch different things.

They notice when a correspondent starts asking more questions. When a market-maker’s inventory drops. When settlement times lengthen. These aren’t formal events. They’re signals that relationships are being recalibrated—and that the liquidity assumed to be unconditional may now come with conditions not yet recognized.

They test assumptions under execution, not just on screens. They model how much of a position could realistically exit in a day, a week, under stress. They recognize that liquidity is a function of size, timing, and market conditions—not just bid-ask spreads.

And they don’t assume liquidity will be there when they need it.

📌 Key Takeaways:

- 1️⃣ Liquidity withdrawal is behavioral, not structural—providers pull back incrementally through selective spread widening, correspondent de-risking, and conditional depth provision.

- 2️⃣ Three forces drive withdrawal: geopolitical fragmentation making relationships conditional, regulatory ambiguity creating costs, and capital efficiency pressures reducing marginal client support.

- 3️⃣ Standard metrics (LCR, bid-ask spreads, volumes) look stable while provider behavior shifts—by the time dashboards show stress, relationships have already changed.

- 4️⃣ Execution risk exceeds mark-to-market risk for concentrated positions—liquidity impact can double losses when forced selling meets thin markets.

- 5️⃣ Recognition requires watching provider behavior (inventory levels, quoting patterns, relationship signals) rather than waiting for metric confirmation.

Liquidity withdrawal doesn’t announce itself with a freeze. It happens in increments—rational, quiet, almost polite.

By the time it shows up in formal metrics, the most consequential choices have already been made.

Frequently Asked Questions

For readers seeking clarity on how to recognize liquidity withdrawal before metrics confirm it:

How is behavioral liquidity withdrawal different from a traditional liquidity crisis?

Traditional liquidity crises are dramatic and visible—spreads blow out, markets freeze, funding dries up. Behavioral withdrawal is incremental and quiet—market-makers reduce inventory by 20%, correspondents tighten documentation for certain corridors, dealers widen spreads selectively. Each move is individually rational and barely noticeable. The infrastructure still works; what’s changing is how providers choose to use it. By the time it shows up in standard metrics, months of behavioral adjustment have already occurred.

What early warning signals indicate liquidity providers are pulling back?

Watch for operational friction that feels isolated but forms a pattern: correspondents asking more questions or processing transactions more slowly; market-makers quoting tighter size limits or stepping away during volatility; settlement times lengthening for certain currencies or corridors; documentation requirements increasing without formal policy changes. These aren’t events—they’re behavioral signals that relationships are being recalibrated and liquidity is becoming more conditional.

Why don’t standard liquidity metrics (LCR, NSFR, bid-ask spreads) capture this risk?

Because they measure outcomes, not behavior. LCR tells you whether you can survive regulatory stress scenarios—not whether counterparties will still transact with you during that stress. Bid-ask spreads show what dealers quote at normal size—not what happens when you need ten times that size. Trading volumes stay elevated, but depth at the size and timing you need may have disappeared. Behavioral shifts precede metric changes by months, so governance sees the withdrawal only after it’s already well advanced.

How should institutions test liquidity assumptions if metrics look stable?

Test execution, not just pricing. Model market impact for concentrated positions—estimate how much you could realistically exit per day under stress. Watch provider behavior (inventory levels, quoting patterns, relationship signals) as leading indicators. Scenario-test what happens if multiple liquidity sources become conditional simultaneously. Recognize that liquidity is a function of size, timing, and relationships—not just what appears on screens.

Next in series: Why Wrong-Way Risk Is Worse Than We Admit

When exposure peaks exactly as counterparty capacity weakens, and why standard models consistently underestimate this structural vulnerability.

Posts like this are written for risk professionals who need to see patterns before metrics confirm them. Subscribe to receive new posts from The Risk Philosopher directly.

Related Reading:

- Part 2 - Geopolitics Is No Longer a Scenario

- Part 1 - Why I’m Concerned About Correlation Regimes

- Explore Emerging Risks

Liquidity isn’t what the market quotes. It’s what the market will execute when you actually need it.