The Compliance Trap: When Risk Functions Optimize for the Wrong Thing

Part 2 - Organizations measure what's unambiguous—control completeness, regulatory adherence, audit findings. Strategic risk identification has none of this clarity. So risk functions optimize for what generates visible returns: compliance excellence over strategic foresight.

Risk Judgment Series

How Risk Teams Actually Fail

Risk functions are designed with sound logic—independence, expertise, board access. Then reality surfaces predictable failure patterns. This series examines how organizational structure, not incompetence, systematically undermines risk teams. Part 2 of 6.

The CRO gets high marks for regulatory completeness. Zero control gaps. Clean audit findings. Flawless documentation across every framework the regulators care about.

The same quarter, a strategic risk that should have been flagged six months earlier surfaces through crisis. Market conditions shifted. The business model assumption that looked solid two years earlier stopped working last quarter. The data was there. The incentive to elevate it wasn’t.

Nobody connects the dots during the performance review.

One failure was measured. The other wasn’t.

This isn’t about incompetent risk teams or indifferent leaders. It’s about what organizations actually reward. Risk functions face asymmetric incentives: compliance failures are visible, punished, and career-ending. Strategic insight failures are invisible until crisis—and by then, everyone’s confused about what went wrong.

The rational response? Optimize for what gets measured.

I’ve watched this pattern repeat across industries, company sizes, and governance maturity levels. The mechanism is structural, not behavioral.

The Incentive Asymmetry

Risk functions operate inside a performance environment with brutally clear signals about what matters.

Miss a regulatory filing deadline: escalation to the board, remediation plans, performance improvement discussions. The control gap gets documented, tracked, and becomes part of your permanent record. Regulators notice. Audit committees ask questions. Someone’s accountability gets clarified very quickly.

Miss an emerging strategic threat: silence. The risk doesn’t announce itself with a deadline. It doesn’t trigger a compliance workflow. It doesn’t generate an audit finding. By the time it surfaces as crisis, the moment when it should have been flagged is months or years in the past—and nobody can reconstruct who should have seen it when.

The asymmetry is structural. Compliance failures have clear attribution, defined timelines, and unambiguous ownership. Strategic insight failures are diffuse, retrospective, and easy to rationalize as “nobody saw it coming.”

So risk professionals learn what their organizations actually care about—not from strategy documents or leadership speeches, but from what generates consequences.

And the lesson becomes unambiguous: regulatory completeness is career-preserving. Strategic foresight is career-neutral until proven otherwise.

The Optimization Pattern

I’ve watched risk functions start with genuine ambition to identify emerging threats early. The mandate says “strategic risk oversight.” The org chart says “enterprise-wide visibility.” The job descriptions emphasize “forward-looking analysis.”

Then performance cycles happen. Compensation reviews. Audit findings. Board questions.

What gets discussed? Control documentation. Regulatory submissions. Framework compliance. The quarterly risk report that took three weeks to compile and seven rounds of review to finalize.

What doesn’t get discussed? The strategic analysis that suggested the industry’s pricing model might be unsustainable. The concern about dependency concentration that didn’t fit the risk register format. The pattern someone noticed but couldn’t quantify in a way that survived committee review.

The optimization is rational and invisible. Risk professionals don’t announce “I’m going to stop thinking about strategic threats and focus on compliance documentation.” They just gradually allocate time and attention to what generates feedback, recognition, and protection from criticism.

The risk function adds headcount for regulatory reporting. Builds more sophisticated control inventories. Implements new frameworks every time a regulator suggests one. Gets praised for audit readiness and documentation quality.

Meanwhile, the capacity for strategic risk sensing quietly erodes—not because anyone decides to abandon it, but because there’s no time left after handling what actually gets measured.

The Measurement Trap

Organizations measure what’s legible and unambiguous. Control frameworks have clear requirements. Regulatory submissions have defined formats and deadlines. Audit findings have explicit criteria for closure.

Strategic risk identification has none of this. When did you know? What should you have flagged? How certain did you need to be before escalating?

Nobody knows.

So organizations default to measuring what can be measured: control coverage, documentation completeness, regulatory adherence, audit findings remediation speed. The risk function’s performance gets evaluated on the quality of its compliance reporting, not the quality of its strategic judgment.

I’ve watched boards ask detailed questions about control gaps and spend three minutes on the “emerging risks” section of the quarterly report—which itself is usually a static list that gets updated twice a year whether anything changes or not.

The message is clear even when it’s unspoken: we have sophisticated measurement for compliance, and vague hope for strategic insight.

Risk functions learn to invest energy where investment generates visible returns. That means comprehensive control inventories, detailed regulatory tracking, and documentation systems that can survive audit scrutiny.

It doesn’t mean spending three days analyzing whether a shift in customer behavior might indicate business model stress. That analysis doesn’t fit the reporting template. Nobody asked for it. And if you’re wrong, it just looks like distraction from the compliance deliverables everyone’s actually tracking.

“Organizations get the risk oversight they incentivize. Most just don’t realize what they’re actually measuring.”

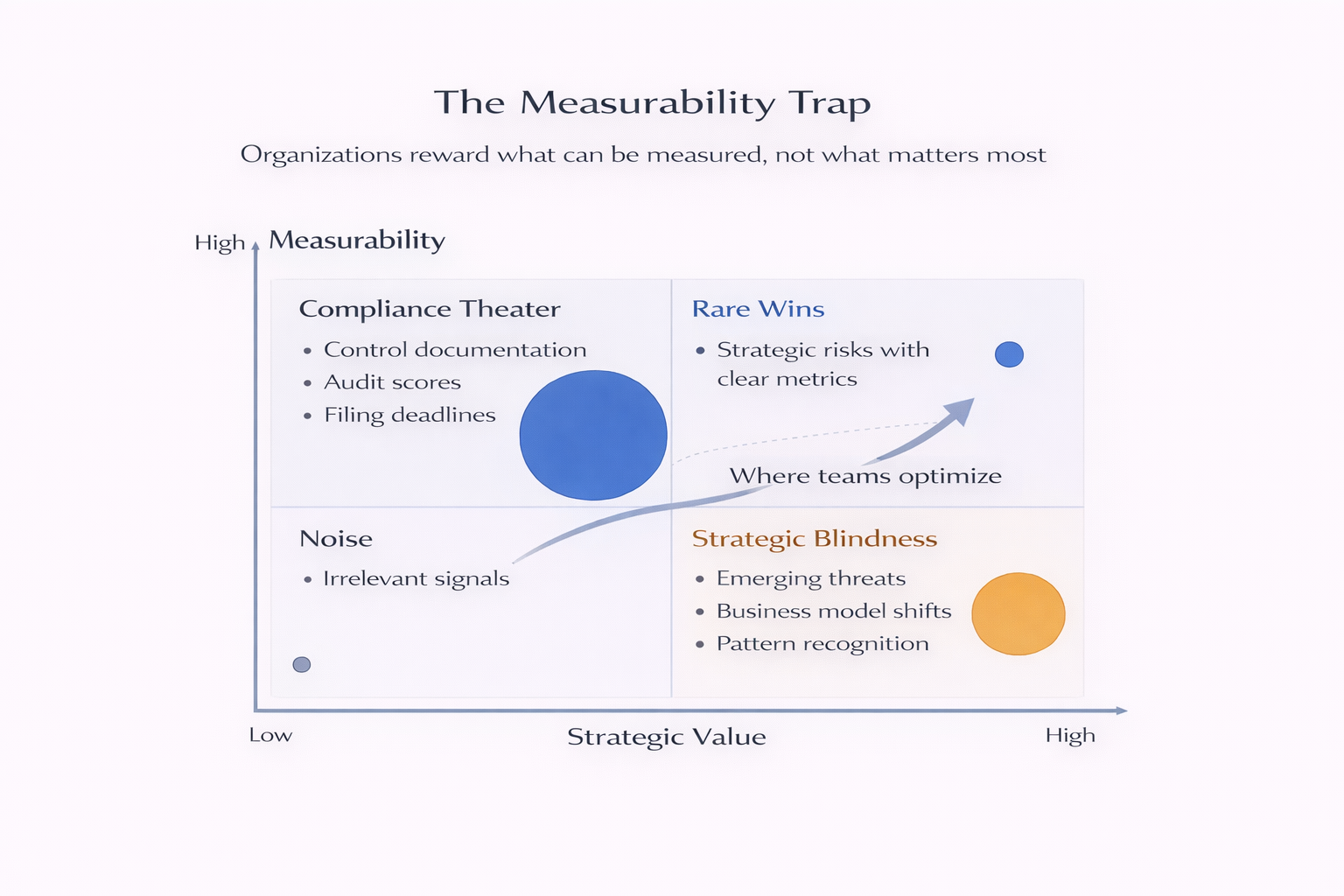

The Measurability Trap

Organizations measure what's unambiguous—control completeness, regulatory adherence, audit findings. Strategic risk identification has none of this clarity. So risk functions optimize for what generates visible returns: compliance excellence over strategic foresight.

The Consequence

The consequence isn’t that risk teams become lazy or indifferent. It’s that they become reporting factories.

I’ve watched highly capable risk professionals spend 70% of their time producing documentation that satisfies audit and regulatory requirements—and then wonder why they don’t have bandwidth for strategic analysis.

“The consequence isn’t that risk teams become lazy. It’s that they become reporting factories.”

The risk function grows. More people get added to handle the expanding compliance workload. Job descriptions emphasize regulatory expertise, control frameworks, and audit liaison. The team’s skills optimize for what the performance system demands: people who can navigate regulatory requirements, produce clean documentation, and manage control inventories efficiently.

What doesn’t get hired for: people who can sense strategic inflection points before they become obvious. People who can sit with ambiguity long enough to identify emerging patterns. People whose instinct is to ask “what are we missing?”—rather than “did we file everything on time?”

Not because organizations don’t value strategic insight—they do. But when your performance system rewards compliance excellence and doesn’t penalize strategic blindness until after crisis, you get professionals who are excellent at compliance.

And when crisis hits, everyone asks why the risk function didn’t see it coming.

The risk function was doing exactly what the measurement system told them to do. They just didn’t realize that “excellent at compliance” and “good at identifying emerging strategic threats” are almost entirely different skill sets—requiring different people, different processes, and different performance incentives.

Organizations assumed the same function could do both. The measurement system ensured they’d optimize for one and deprioritize the other.

📌 Key Takeaways:

- 1️⃣ Compliance failures have clear attribution and consequences. Strategic insight failures are diffuse and retrospective—easy to rationalize as “nobody saw it coming.”

- 2️⃣ Risk professionals optimize rationally. They allocate time to what generates feedback, recognition, and protection from criticism.

- 3️⃣ Organizations measure what’s unambiguous. Control completeness has clear metrics. Strategic foresight doesn’t—so it gets deprioritized.

- 4️⃣ The consequence is skill mismatch. Performance systems that reward compliance excellence produce teams excellent at compliance—not strategic risk sensing.

The Pattern Isn’t Fixable Through Better Goal-Setting

The pattern is structural, not fixable through better goal-setting or leadership emphasis on “strategic thinking.” When performance systems reward compliance completeness and audit cleanliness, risk functions will optimize for compliance completeness and audit cleanliness.

When regulatory failures end careers and strategic blindness ends quietly, teams will prioritize regulatory compliance.

When the only questions asked during board meetings are “Did we miss any control requirements?” and never “Did we identify emerging threats early enough?”, functions will optimize for control documentation.

The risk function becomes what the measurement system says it should become—even when that’s the opposite of what the organization actually needs.

Organizations get the risk oversight they incentivize. Most just don’t realize what they’re actually measuring.

Frequently Asked Questions

For readers seeking quick answers to common questions about compliance optimization and risk function performance measurement:

Don’t risk functions have mandates that include both compliance and strategic risk oversight?

They do—but mandates don’t determine behavior, incentives do. When performance reviews emphasize regulatory completeness and audit findings, while strategic insight failures remain invisible until crisis, teams rationally optimize for what’s measured. The mandate says both; the measurement system says one matters more.

Can’t organizations simply add strategic risk metrics to their performance systems?

Strategic risk identification resists easy measurement. When did someone know? What should they have flagged? How certain did they need to be? These questions have no clear answers before crisis provides retrospective clarity. Organizations default to measuring what’s unambiguous—which is why compliance metrics dominate.

Is this pattern unique to highly regulated industries?

No. I’ve observed it across regulated and unregulated sectors. Any organization with audit functions, control frameworks, and compliance requirements creates the incentive asymmetry. The pattern is most visible in financial services, but the mechanism operates wherever regulatory adherence generates clearer consequences than strategic foresight.

What signals indicate a risk function has become a reporting factor?

Risk professionals spending most of their time on documentation and regulatory submissions. Headcount growth focused on compliance expertise rather than strategic sensing. “Emerging risks” sections of reports that remain static for months. Board meetings that scrutinize control gaps but spend minimal time on forward-looking analysis.

Continue the Series

This is Part 2 of a 6-part series examining how risk teams fail through structural design, not incompetence.

Next: Why technical expertise becomes a communication liability—and how specialization creates the credibility gap that marginalizes risk functions.

New posts every week. Unsubscribe anytime.

Related Reading

- When Independence Becomes Isolation: How the structural separation designed to empower risk teams systematically cuts them off from the early, messy signals they need.

- How Incentives Quietly Shape What Gets Taken Seriously: Why organizations pay attention to risks that fit existing incentive structures while strategic threats remain invisible until after they materialize.

- When Governance Becomes a Substitute for Judgment: How organizations build elaborate risk frameworks that create the appearance of control while actual judgment quietly disappears.

You can have independence or you can have early information. The org chart pretends you can have both.