Where Risk Becomes Invisible

Part 3 - Risk accumulates in the spaces between frameworks—where no function owns it, where pieces are visible but the whole never crystallizes. How organizational structures create blind spots faster than governance can detect them.

How Organizational Structures Create Blind Spots Faster Than Frameworks Can Detect Them

📊 EMERGING RISKS SERIES: Why The Old Tools Fail Quietly — Part 3 of 4

In Parts 1 and 2, we examined how AI risk escapes technical framing and why governance can't keep pace with risk velocity. This post explores a deeper problem: how organizational structures create blind spots that multiply risk faster than frameworks can detect.

I. The Pattern That Keeps Repeating

What Frameworks Miss by Design

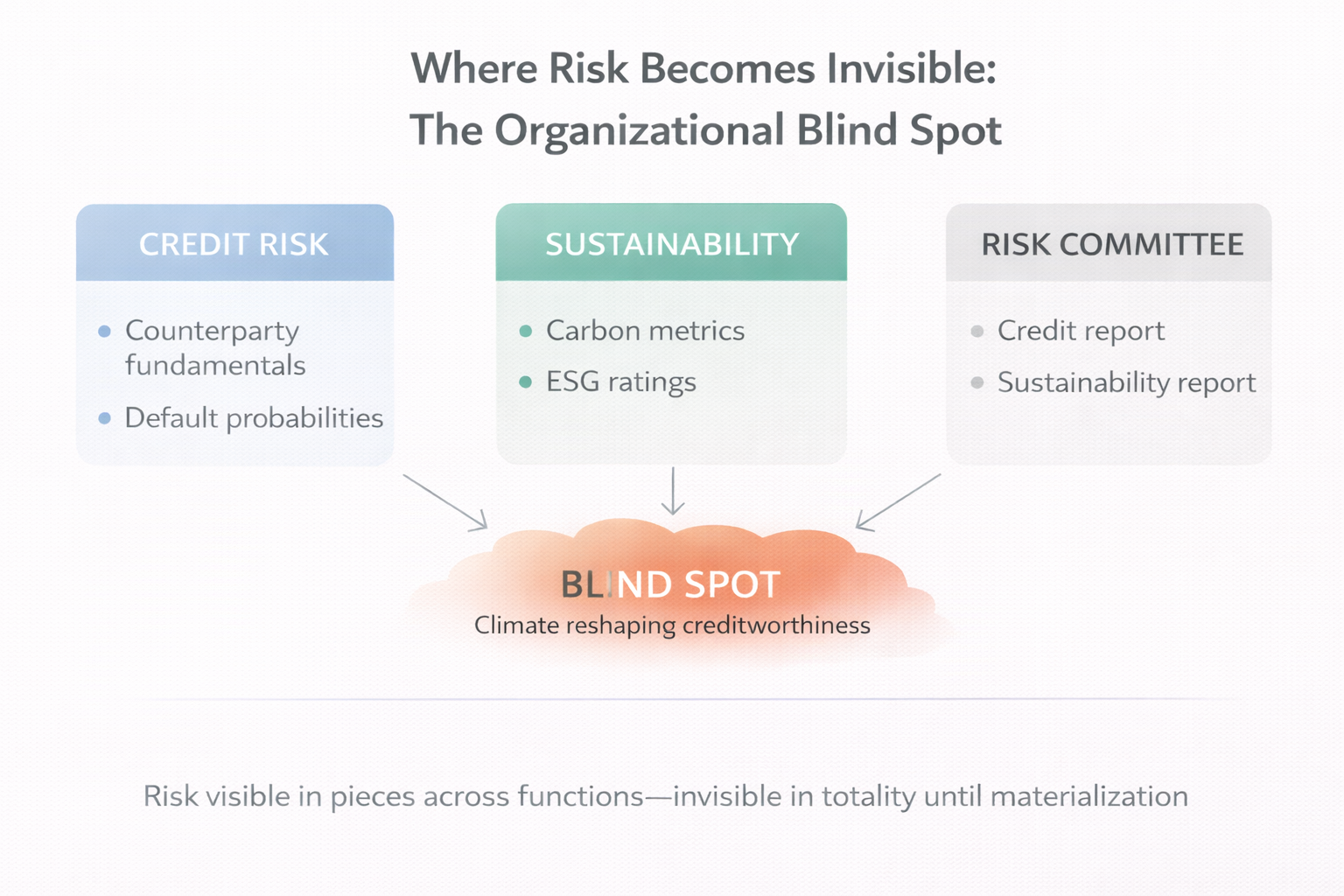

A large financial institution discovered something unsettling during a routine audit. Over eighteen months, their climate-related credit exposures had grown by forty percent. Not because they’d taken on riskier borrowers—but because borrowers’ risk profiles had shifted while the bank’s frameworks looked elsewhere.

The exposure was hiding in plain sight. Credit teams tracked counterparty risk. Sustainability teams tracked carbon metrics. Risk committees reviewed both reports separately. But no one was watching how climate volatility was quietly reshaping creditworthiness—margin compression from volatile input costs, unplanned capital expenditure, demand shocks in climate-sensitive sectors.

By the time someone connected the dots, the bank couldn’t reprice quickly enough. Markets had already moved. The exposure was locked in.

This isn’t a story about negligence. It’s a story about structure.

I’ve watched variations of this pattern unfold across different organizations and different risk domains. The details change, but the mechanism stays the same: risk accumulates in the spaces between frameworks—where no single function owns it, where it doesn’t fit existing categories, where pieces are visible but the whole never crystallizes.

Most organizations don’t fail because they ignore risk. They fail because risk forms outside their field of vision, then compounds faster than their systems can adjust.

II. Where Vision Ends

How Organizational Architecture Creates Invisibility

The risks that do the most damage aren't usually the ones no one thought of. They're the ones organizational structures aren't built to surface.

This invisibility isn't random. It's produced by design choices that made perfect sense when implemented—choices about how to organize functions, define ownership, structure reporting, and allocate accountability.

Frameworks create boundaries to make risk manageable. Credit risk sits here. Market risk sits there. Operational risk has its own taxonomy. This works exceptionally well for risks that respect those boundaries. It fails when risk doesn't.

I've sat in rooms where three different teams were tracking pieces of the same emerging risk, none realizing their exposures were connected. Not because they weren't competent—because the organizational chart said these were separate domains.

Model boundaries narrow the frame. Every risk model simplifies reality to make risk measurable. They exclude tail interactions, feedback loops, behavioral adaptation. This isn't a flaw—it's the price of tractability. But blind spots emerge at the edges, where assumptions end and reality continues.

Functional ownership fragments attention. Risk ownership gets allocated by type: credit, market, liquidity, operational, compliance. Emerging risks rarely respect those boundaries. AI risk interacts with conduct and credit outcomes. Climate transition risk interacts with asset values and capital adequacy. Geopolitical risk interacts with liquidity, sanctions, and operational continuity. When no single function owns the interaction, the risk remains fragmented—visible in parts, never in totality.

Regulatory perimeters define what gets attention. Supervisory frameworks specify what must be monitored, reported, governed. They also—unintentionally—define what receives less focus. Risks that sit outside formal scope, cut across jurisdictions, or evolve faster than guidance tend to remain underdeveloped internally, even when they're strategically material.

Data asymmetry determines what surfaces. What can be measured dominates what gets discussed. Early signals of emerging risk are often qualitative, fragmented, noisy. They don't travel well through formal reporting channels. By the time data becomes clean enough to satisfy governance requirements, the underlying risk may have already shifted.

III. Why Invisibility Multiplies Risk

When Blind Spots Compound Faster Than Frameworks Adapt

In earlier risk environments, blind spots were survivable. Risks moved slowly enough that even delayed recognition left time to respond. They arrived sequentially, giving organizations space to address them one at a time.

That margin has disappeared.

Today’s most consequential risks share three characteristics that make blind spots far more dangerous:

They interact. Risks no longer arrive in isolation. They collide, amplify each other, create second-order effects that weren’t in anyone’s scenario. A geopolitical shift becomes a sanctions issue becomes a liquidity stress becomes an operational continuity problem—all in the same quarter.

When risks interact before they’re recognized, the compounding happens invisibly. By the time governance sees the combined exposure, it’s already material.

They accelerate. Materialization often occurs faster than governance cycles. What starts as a weak signal becomes a developed risk before the next committee meeting. The tempo mismatch we examined in Part 2 makes blind spots more dangerous—there’s less margin for delayed detection.

They transform. By the time a risk is recognized and named, it may no longer resemble its initial form. This makes backward-looking frameworks particularly vulnerable. They’re calibrated to detect the last version of a risk, not its current mutation.

Climate risk is the clearest demonstration of how this works in practice.

IV. How Climate Risk Forms in the Blind Spots

The Timing Problem Most Frameworks Miss

Most climate risk discussions still start in the wrong place. They begin with transition plans, alignment statements, net-zero commitments. But from a risk perspective, climate shows up somewhere more immediate—and more dangerous.

It shows up when a borrower’s cashflows weaken before a loan can be repriced. When collateral values shift faster than credit models adjust. When insurance quietly disappears. When markets move on expectation while balance sheets move on contract.

Climate risk is fundamentally a timing problem. And timing problems don’t wait for transition plans to mature.

Markets reprice on expectation. Balance sheets reprice on contract. That mismatch is where climate risk does its quiet work.

Market prices can move in weeks—sometimes days—on policy signals, weather events, technological shifts, or changes in sentiment. Balance sheets, by contrast, are constrained by fixed-rate lending, long tenors, illiquid collateral, relationship-based exposures, slow-moving governance cycles.

When repricing happens faster than risk mitigation, exposure accumulates silently. This is why climate risk often feels abstract—until it suddenly isn’t.

Second-order effects are where frameworks go blind. Climate risk rarely hits first-order assumptions cleanly. Its most material impacts arrive through channels models don’t capture well.

On the credit side: margin compression from volatile input costs, unplanned capital expenditure to meet regulatory requirements, demand shocks in climate-sensitive sectors, shortened business planning horizons.

On the collateral side: assets becoming harder to insure, properties exposed to repeated disruption, infrastructure whose useful life shortens faster than depreciation schedules assume.

On the liquidity side: funding spreads widening, depositor behavior shifting, market access tightening during periods of climate-related uncertainty.

None of this requires perfect data or twenty-year forecasts. It requires recognizing how quickly confidence and pricing can move—and how slowly balance sheets follow.

The blind spot forms at the intersection. Credit teams see counterparty fundamentals. Sustainability teams track emissions. Risk committees review both. But the interaction—how climate volatility reshapes creditworthiness faster than frameworks adjust—sits between functions.

By the time someone asks “how much of our credit deterioration is climate-linked?”, the exposure is already on the books. The repricing window has closed.

This is the pattern: risk visible in pieces, invisible in totality, materializing faster than organizational structures can synthesize the fragments.

V. Where Else This Pattern Appears

Geopolitics, Technology Dependencies, and Other Structural Gaps

Climate demonstrates the mechanism clearly, but it’s far from the only domain where blind spots multiply risk.

Geopolitical assumption drift creates similar dynamics. Organizations built operating models assuming enforceability, capital mobility, regulatory alignment. Those assumptions are eroding—not through single events, but through gradual fragmentation.

Sanctions risk is no longer a compliance checklist. It’s dynamic, politically mediated, unevenly enforced. Exposure arises from spillover, interpretation, counterparty behavior under pressure. But it sits between legal, treasury, and credit functions. The synthesis happens too late.

Technology dependency concentrations hide in vendor relationships, cloud infrastructure, data pipelines. Each dependency looks manageable in isolation. But when they intersect—when a cloud provider has a sanctions issue, or a critical vendor faces geopolitical disruption—the compound exposure emerges suddenly.

No single function owns “technology dependency risk across geopolitical fault lines.” So it remains fragmented until it materializes.

Regulatory divergence creates blind spots as jurisdictions move in different directions. What’s acceptable in one market becomes challenged in another. Group-level consistency, once stabilizing, increasingly generates friction. The risk sits between compliance, legal, and business strategy—visible to each, owned by none.

The pattern repeats: organizational structures that worked when risks stayed in their lanes now create blind spots when risks intersect.

"The most dangerous risks aren't always the ones rated too low on the register. They're the ones forming quietly in the spaces between it—where visibility is weakest and response is slowest."

VI. Why Strengthening Frameworks Isn’t Enough

The Epistemic Limit of Organizational Risk Management

The instinctive response to blind spots is to improve frameworks: add categories, refine taxonomies, enhance reporting, expand scenarios, increase cross-functional oversight.

These steps matter. But they don’t eliminate blind spots.

Frameworks, by design, codify what’s already understood. They stabilize governance. They trade completeness for usability. They excel at managing known risks within defined boundaries.

They struggle with emergent interactions happening in real-time across those boundaries.

This isn’t a governance failure. It’s an epistemic limit. No framework can fully capture a dynamic, interconnected risk environment in real-time. The moment you define categories, you create edges. The moment you assign ownership, you create gaps. The moment you build models, you create boundaries.

I’ve watched organizations invest heavily in better frameworks while blind spots continued forming—not because the frameworks were poorly designed, but because the nature of risk had changed faster than the structures designed to surface it.

You can have robust governance, sophisticated models, and disciplined risk culture—and still be exposed to risks your organization isn’t structurally equipped to see early.

VII. What This Means for Risk Leaders

Navigating Structural Invisibility

The question isn’t how to eliminate blind spots. It’s how to govern effectively while knowing they exist.

Recognize where blind spots form. They emerge predictably at organizational interfaces: between functions, between first-order and second-order effects, between regulatory perimeters, between what’s measured and what matters, between model assumptions and messy reality.

If you know the structural features that create invisibility, you know where to look.

Watch for interaction effects. When separate teams start reporting related but disconnected signals, that’s often a blind spot forming. Climate stress in one portfolio, insurance withdrawal in another, collateral repricing in a third—all linked, none synthesized.

The pattern appears before the risk fully materializes. The question is whether governance has space to notice.

Question what’s not being discussed. The risks that dominate committee agendas are usually well-understood and well-managed. The ones that don’t make the agenda—because they sit between categories, because data is messy, because ownership is unclear—are often where real exposure is building.

Pay attention to what’s consistently deferred, what’s “on the radar but not urgent,” what’s “being monitored” without clear ownership.

Build judgment in the gaps. Process works well for known risks. It fails in the spaces between. That’s where judgment matters most—the ability to synthesize fragments, recognize patterns before they’re named, act on incomplete information when waiting for clean data means waiting too long.

This can’t be proceduralized. It has to be preserved deliberately.

Accept the discomfort of incomplete vision. The instinct is to want full visibility, complete coverage, no gaps. That’s not achievable when risk moves faster than frameworks evolve and interacts in ways structures weren’t designed to capture.

The work isn’t eliminating uncertainty. It’s governing effectively while acknowledging how much sits outside the frame.

📌 Key Takeaways:

- 1️⃣ Risk doesn't fail because organizations ignore it—it accumulates in the spaces between frameworks where structures create invisibility

- 2️⃣ Blind spots form predictably: at functional boundaries, between first and second-order effects, in model edges, across regulatory perimeters

- 3️⃣ Today's risks interact, accelerate, and transform faster than organizational structures can synthesize fragmented signals

- 4️⃣ Climate risk demonstrates the pattern: timing mismatches create exposure that's visible in pieces but invisible in totality until too late

- 5️⃣ Strengthening frameworks helps but doesn't eliminate blind spots—they're a structural feature, not a governance failure

Closing Note

Blind spots aren’t the exception in modern risk management. They’re the norm.

Every organizational boundary creates potential invisibility. Every framework creates edges. Every model creates assumptions that don’t quite match reality. Every ownership structure creates gaps.

This was manageable when risks stayed in their lanes, moved slowly enough for delayed recognition, and materialized in ways that matched existing categories.

Those conditions no longer hold.

What’s changed isn’t that organizations have gotten worse at seeing risk. It’s that risk increasingly forms in ways organizational structures weren’t designed to surface—across functions, between categories, in interactions rather than isolation.

The most dangerous exposures aren’t always the ones rated too low on the risk register. They’re the ones forming quietly in the spaces between it, where visibility is weakest and response is slowest.

By the time they become obvious, they’re usually no longer emerging risk. They’re already impact.

Frequently Asked Questions

For readers seeking quick answers to specific questions about organizational blind spots and structural risk invisibility:

What are organizational blind spots in risk management?

Organizational blind spots are risks that exist and are material but remain outside the field of vision created by existing governance, models, and reporting structures. They're not unknown risks—they're structurally invisible risks that fall between frameworks, functions, or regulatory perimeters. Risk is present and accumulating, but organizational architecture prevents it from crystallizing as an "owned" risk that triggers governance attention.

Why do blind spots form even in well-governed organizations?

Blind spots are an emergent property of organizational structure, not a governance failure. They form because of design choices that make risk management tractable: model boundaries that simplify reality, functional ownership that allocates risk by type, regulatory perimeters that define scope, and data requirements that favor what's measurable. These features work well for risks that respect boundaries but create invisibility when risks interact across categories or materialize between functions.

How do blind spots multiply risk?

Blind spots multiply risk through delayed recognition and compressed response time. When risk accumulates invisibly, it compounds before governance sees the full picture. By the time fragments are synthesized, materialization is often already underway and response options have narrowed. In today's environment where risks interact, accelerate, and transform quickly, this delay converts manageable emerging risk into developed exposure.

Why is climate risk a blind spot for many organizations?

Climate risk demonstrates blind spot formation clearly because it operates through timing mismatches and second-order effects that sit between traditional functions. Markets reprice climate exposure based on expectations while balance sheets reprice based on contracts—creating a lag where risk accumulates. Credit teams see counterparty fundamentals, sustainability teams track emissions, but the interaction—how climate reshapes creditworthiness—often sits between them until exposure is already locked in.

How are blind spots different from unknown risks?

Unknown risks are genuinely outside current imagination—rare "black swans." Blind spots are different: the risk elements are known and visible in pieces, but organizational structures prevent synthesis. Multiple teams may be tracking related signals without realizing they're connected. The risk isn't absent from the organization—it's fragmented across boundaries in ways that prevent full recognition until it materializes.

What should risk leaders do about structural blind spots?

Recognize that blind spots can't be eliminated—they're structural features of how organizations manage complexity. Instead, focus on where they predictably form: at functional interfaces, between first and second-order effects, in model assumptions, across regulatory perimeters. Watch for interaction effects when separate teams report disconnected but related signals. Question what's consistently not discussed in governance. Build judgment to act on incomplete information in the gaps where process can't reach. Accept that complete visibility isn't achievable when risk moves and interacts faster than structures evolve.

Next in this series: Part 4: After The Old Tools—What Comes Next

Subscribe to The Risk Philosopher to follow this 4-part series examining how traditional risk frameworks fail to keep pace with reality—and receive new posts on risk judgment and emerging risks.

Related Reading:

In This Series:

- Part 1: AI Risk Is Not a Technology Problem

- Part 2: The Temporal Mismatch—When Risk Moves Faster Than Governance

- Part 4: After The Old Tools—What Comes Next (Coming soon)

Emerging risk rarely announces itself. It accumulates where visibility is weakest—and acts where response is slowest.