Why I’m Concerned About Correlation Regimes

Part 1 - Portfolio diversification benefits are eroding as correlation regimes shift faster than risk models can capture. When assets move in lockstep under stress, balanced portfolios become concentrated positions—and governance structures can't track changes.

📊 EMERGING RISKS SERIES: What I'm Watching Now — Part 1 of 5

This post is part of a series on current portfolio risk patterns that concern experienced CROs—not event analysis, but practitioner intelligence on market risks forming before they're widely recognized.

In this post: why diversification assumptions in risk management are breaking down faster than correlation models acknowledge, and what it means for asset allocation when correlation regimes shift in hours while governance operates in quarters.

For the past eighteen months, I’ve been watching something that should concern every CRO: diversification benefits are eroding faster than risk models acknowledge.

Portfolios designed for balance—60/40 allocations, cross-asset hedges, carefully calibrated exposure mixes—are increasingly moving as single positions under stress. Assets that historically zigged and zagged now mostly just zig.

This isn’t a replay of 2008 or March 2020. It’s something structurally different in how markets are behaving. And the correlation assumptions built into risk frameworks aren’t keeping pace with the change.

What concerns me is not that stress creates co-movement. That’s expected. What concerns me is that the conditions for regime shifts are intensifying—and most governance structures won’t recognize the shift until well after it’s already occurred.

Why This Matters Now

I’ve watched the assumption that correlation is stable—or at least predictable in its instability—break down repeatedly. Not through single dramatic events, but through accumulating evidence that the relationships markets are pricing today are not the relationships that will hold under pressure.

Portfolios stress-tested with historical correlation matrices look robust. Then stress arrives, and the matrix itself shifts. What looked like 0.3 correlation in calm markets becomes 0.8 or 0.9 under pressure. Diversification that existed on paper disappears exactly when it’s needed most.

The problem is not that this happens. The problem is how quickly it happens, and how persistently the new regime can hold once established.

Standard risk models treat correlation as a parameter to calibrate. What I’m seeing suggests it’s closer to a regime that shifts—sometimes abruptly, sometimes irreversibly—and that the triggers for those shifts are becoming more frequent.

What‘s Driving the Regime Change

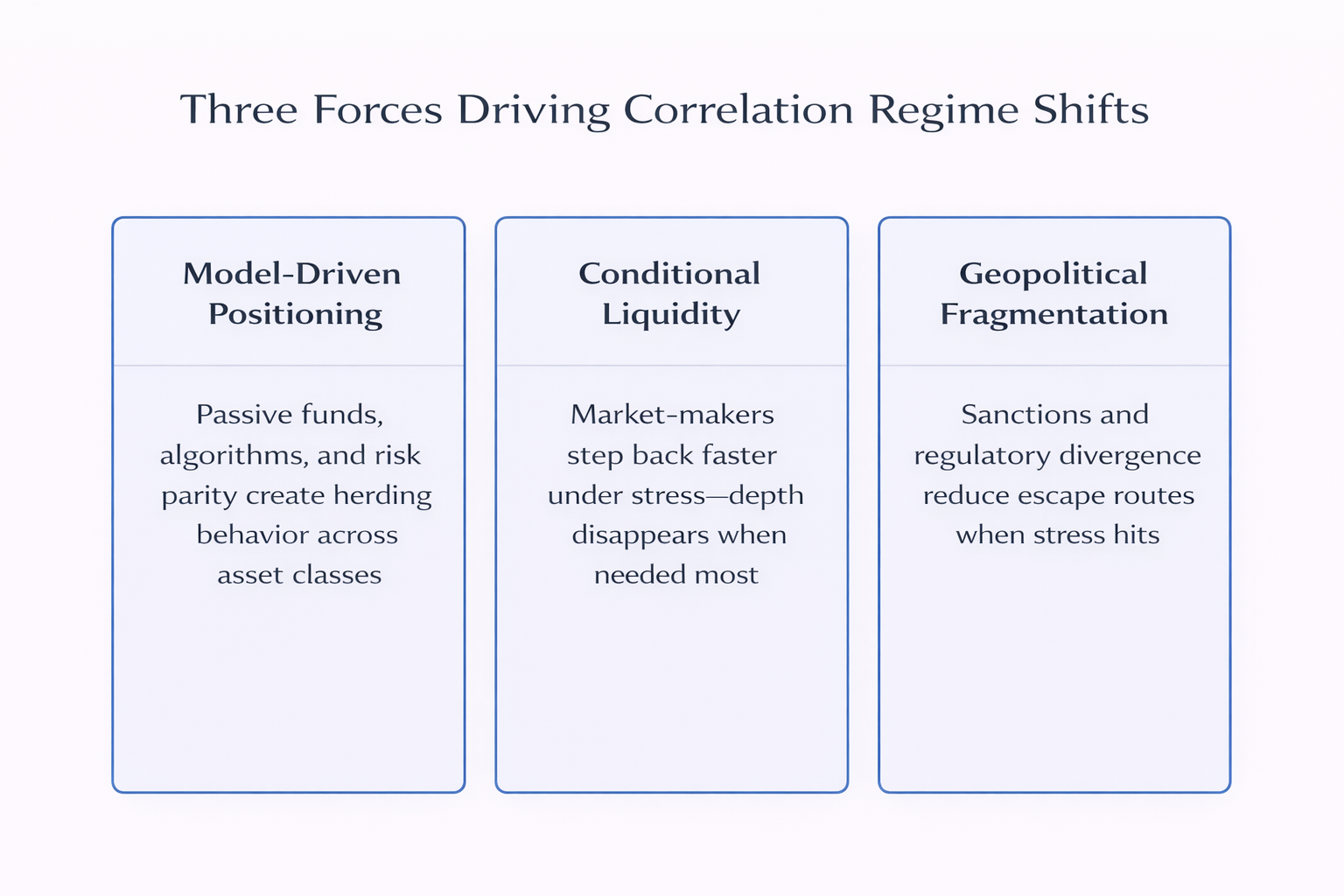

Three structural forces are changing how correlation behaves, and they’re all intensifying.

Model-driven positioning has become market structure. Passive strategies, algorithmic trading, risk parity funds, volatility targeting—these aren’t marginal players anymore. They’re the market. And they respond to the same signals in similar ways.

When volatility spikes, these strategies reduce exposure across asset classes simultaneously. When momentum builds, they chase it in parallel. The effect is that markets which should move independently increasingly move together, because the capital allocating across them is following the same logic.

I’ve watched portfolios that looked diversified across equities, credit, and rates all reprice in the same direction within hours, not because fundamentals changed in all three domains, but because positioning unwound in all three at once.

That’s not correlation in the statistical sense. It’s herding. But it shows up in your portfolio the same way correlation does—everything moves together, and your hedges stop working.

Liquidity provision has become more conditional. Market-makers and liquidity providers are faster to step back when volatility rises. Bid-ask spreads widen, depth disappears, and the act of trying to rebalance or hedge becomes itself a source of price movement.

This creates feedback loops. Stress reduces liquidity, which amplifies price moves, which triggers more model-driven repositioning, which removes more liquidity. By the time the loop stabilizes, correlation has already shifted to a new regime.

What’s unsettling is how quickly this can happen. Not over weeks or months—over hours. Governance structures built for quarterly reviews and monthly risk committees aren’t designed for risks that materialize and stabilize in a single trading session.

Fragmentation has reduced escape routes. Geopolitical fragmentation, regulatory divergence, and sanctions have made it harder to move capital freely across markets and jurisdictions. Assets that used to offer genuine geographic and regulatory diversification now carry embedded concentration risk—because when stress hits, the number of viable places to move has quietly narrowed.

I’ve seen institutions discover during stress that their “global” portfolio was functionally a regional one, because the routes they assumed would stay open had become conditional on political relationships that were themselves under pressure.

That’s a different kind of correlation risk. Not statistical, but structural. And it doesn’t show up in backtests because the conditions that make it visible are new.

Where This Shows Up

The pattern I’m watching appears in several places, and they’re becoming more common.

Equity and credit moving in lockstep. Historically, equity sell-offs and credit spread widening were related but not perfectly synchronized. There was time to reposition, hedge, or adjust.

I’ve watched that buffer narrow. Equity volatility now transmits into credit spreads faster and more directly. When equity markets reprice risk, credit follows almost immediately—and both hit portfolios that assumed some independence between the two.

For institutions with mixed books, this matters. The diversification benefit that used to come from holding both equities and credit is weakening. Stress scenarios built on historical correlation are understating how much capital is actually at risk when both move together.

Geographic diversification compressing. Institutions build portfolios across regions assuming that local shocks will remain local. Europe, Asia, North America—each with different drivers, different cycles, different policy regimes.

I’ve watched that logic weaken. Policy shocks in one region transmit faster. Trade tensions create synchronized impacts. Sanctions and regulatory fragmentation mean that capital can’t flow as freely to rebalance when one region underperforms.

The result is that portfolios that look geographically diverse on paper are functionally more concentrated than the allocations suggest. And when stress hits, the benefits of that diversity don’t materialize because the transmission channels between regions have become tighter and faster.

Why Governance Struggles to Respond

The challenge is not that risk professionals are unaware of correlation risk. Most frameworks acknowledge it. Stress tests include correlation shocks. Governance papers discuss tail dependence and regime shifts.

The challenge is that recognizing a regime shift requires seeing a pattern that doesn’t yet exist in the data being reported.

By the time correlation changes show up in risk dashboards, they’re already historical. The portfolio has already repriced. The losses have already been realized. The governance conversation is retrospective—why did this happen—rather than prospective—what’s forming now.

I’ve watched risk committees review correlation matrices that looked stable right up until the month they weren’t. The data said everything was fine. Then one stress event shifted the regime, and suddenly the historical calibration was irrelevant.

The question I keep asking is: how do you govern a risk that materializes faster than governance operates?

What I’m Watching For

I don’t claim to predict when correlation regimes will shift. The triggers are too context-dependent, too shaped by positioning and policy and behavioral feedback loops.

What I can do is watch for the conditions that make shifts more likely—and recognize when those conditions are intensifying.

Concentration in model-driven strategies. When passive flows, risk parity positioning, and volatility-targeting strategies are all moving in the same direction, I know that a volatility shock could trigger synchronized repositioning. That doesn’t mean it will happen. It means the fragility is present.

Liquidity provider behavior. When bid-ask spreads widen even in calm markets, when market-makers reduce inventory, when trading volumes stay elevated but depth doesn’t return—those are signals that liquidity provision is becoming more conditional. If stress arrives while providers are already cautious, the amplification will be faster.

Policy and geopolitical friction. When trade restrictions tighten, when sanctions expand, when regulatory regimes diverge—these reduce the number of places capital can move freely. That makes correlation more likely to spike, because there are fewer escape routes when stress hits.

Volatility term structure. When implied volatility in near-dated options rises relative to longer-dated options, it suggests markets are pricing near-term event risk. If that happens while positioning is concentrated and liquidity is conditional, the setup for a regime shift is in place.

None of these signals is decisive on its own. But when multiple signals align, I know the conditions for a correlation regime shift are present. And that changes how I think about portfolio risk, stress testing, and capital buffers.

📌 Key Takeaways:

- 1️⃣ Diversification benefits are eroding faster than risk models acknowledge—portfolios designed for balance increasingly move as single positions under stress

- 2️⃣ Three structural forces drive this: model-driven positioning creating herding, conditional liquidity provision amplifying moves, and geopolitical fragmentation reducing escape routes

- 3️⃣ Correlation regime shifts now happen in hours, not weeks—faster than governance structures are designed to respond

- 4️⃣ Recognition requires watching conditions that precede shifts (positioning concentration, liquidity behavior, policy friction, volatility term structure) rather than waiting for dashboards to confirm changes

- 5️⃣ The practitioners who manage this well recognize that “normal times” are shorter and less stable than they used to be—and act accordingly

What This Means

The practitioners who manage correlation risk well aren’t the ones with the most sophisticated models. They’re the ones who watch for the conditions that precede regime shifts, who ask uncomfortable questions about diversification assumptions before stress forces the answers, and who recognize that by the time correlation changes show up in dashboards, the most consequential decisions have already been made.

Correlation regimes don’t shift on a schedule. They shift when conditions align.

And those conditions are aligning more frequently than they used to.

Frequently Asked Questions

For readers seeking clarity on detecting and responding to correlation regime shifts:

What is correlation risk in portfolio management?

Correlation risk is the danger that assets assumed to move independently will instead move together during stress, eliminating diversification benefits. When correlation regimes shift, portfolios that looked balanced can behave as concentrated positions.

Why is diversification breaking down?

Three structural forces: model-driven markets creating synchronized positioning, conditional liquidity provision amplifying price moves, and geopolitical fragmentation reducing the number of viable places to move capital during stress.

How do you detect correlation regime shifts early?

Watch for conditions that precede shifts rather than waiting for correlation metrics to change: positioning concentration in model-driven strategies, liquidity provider behavior, policy and geopolitical friction, and volatility term structure signals.

What should risk professionals do about correlation risk?

Recognize that correlation regimes shift faster than governance operates. Focus on monitoring conditions that make shifts likely, stress-testing under multiple correlation scenarios, and maintaining flexibility to respond when regimes change rather than relying on historical calibration.

Next in the series: Geopolitics Is No Longer a Scenario

How geopolitical fragmentation has moved from episodic disruption to structural condition, and what that means for the assumptions built into risk frameworks.

Posts like this are written for risk professionals who need to see patterns before metrics confirm them. Subscribe to receive new posts from The Risk Philosopher directly.

Related Reading:

- Read the previous series: “When Risk Stops Behaving”

- Explore Emerging Risks

- About The Risk Philosopher

Diversification is a promise built on assumptions. When the assumptions shift faster than the models, the promise becomes a memory.